Buying an Existing Business: What You Should Know Before Signing on the Dot

.png)

Key Takeaways

Due Diligence is Key: Thoroughly investigate all aspects of the business to uncover potential risks and confirm its value.

Financial Planning is a Must: Secure favorable financing terms and ensure sufficient working capital to support operations and growth.

Preparing for Transition and Negotiation: Carefully plan for a smooth handover and negotiate terms that safeguard the business's future success.

Experience is a key factor when buying an existing business for sale, but many upcoming entrepreneurs don't know most of the ins and outs of what to look for. But that’s normal, and there are many ways to seek advice and help. Some, which are called business brokers, can walk with you throughout each step to help you get the best deal for a fee, while others opt for a lawyer. For free help, check out SBA.gov after reading this guide.

Do you have what it takes to buy an existing business?

Yes. As it may seem scary to buy a business for sale, it's really not that complicated, just like those who buy a house for the first time. They worry about the down payment, the mortgage, and what will happen if stuff breaks in the house, but once all is settled and done and the equity is growing, you sit back and say, "I made a good choice." When it comes down to business, it can be a bit similar but needs more due diligence. In this guide, we will do our best to break down some of the important factors that come before acquiring the business.

What you need to know before buying an existing business?

There are a few things—well, more than a few things—when it comes to starting the process. Below, I listed ten, and to note, there are way more, but it's important to not take on this role on your own. As you will regret anything that comes up after you sign the deal. A business for sale listing will display numbers and a brief description about once you contact the listing broker. They will have you sign an NDA (Non-disclosure Agreement). This protects sellers and the brokers so no deals are done behind their back. Once they are signed, they will present you with the obvious like address, financials, and so on. But that doesn't give you permission to reach out to employees and start asking questions; you need to keep your distance unless told otherwise.

Hiring a business broker can be there step by step and even tell you, "Hey, hold off on this deal; it's not a good deal."

With that being said, let's look at these 10 things you should know before signing the deal.

1. Understanding the Market - Business Purchase Guide

I made this the top priority when acquiring a business for sale, and let me explain why. It takes 3 years to build a business and 3 months to lose it; I learned that the hard way! If you are thinking of taking over someone else's business, make sure you really understand the market. Yes, training that will come with the deal is fine, but is it enough?

For example, here on BizRoutes, we love researching businesses, giving users a bit of understanding about the business listing. It's more than just numbers that are displayed. These are more than just business purchase guides; we call them buyers' guides, which you can find in our BizHub section. The moral is understanding the market info is important when buying a business; it gives you the ability to take that business further than it already is.

2. If Any Financing, What Are the Exact Terms - Financing a Business Purchase

The business you are considering buying is offering financing—Sweet! But don't let that turn a blind eye; financing a business purchase needs careful examination. Like literally, make sure you read the fine print. A few missed payments may be enough for the old owner to take back the business!

So hiring a lawyer to help you read or restructure the terms that will work best for you and the seller is ideal in this case (Don't do this on your own!).

3. Having Working Capital - Avoiding Pitfalls in Business Acquisition

Many new buyers max out everything they got to get the deal done, which is quite impressive, but what happens here is after the business transition and how to avoid pitfalls in business acquisition. These are common mistakes that happen, but I get it; you may think it's fine because you own the business and money will roll in. Advice: don't think that way; think the opposite. What if money doesn't roll in quickly enough?

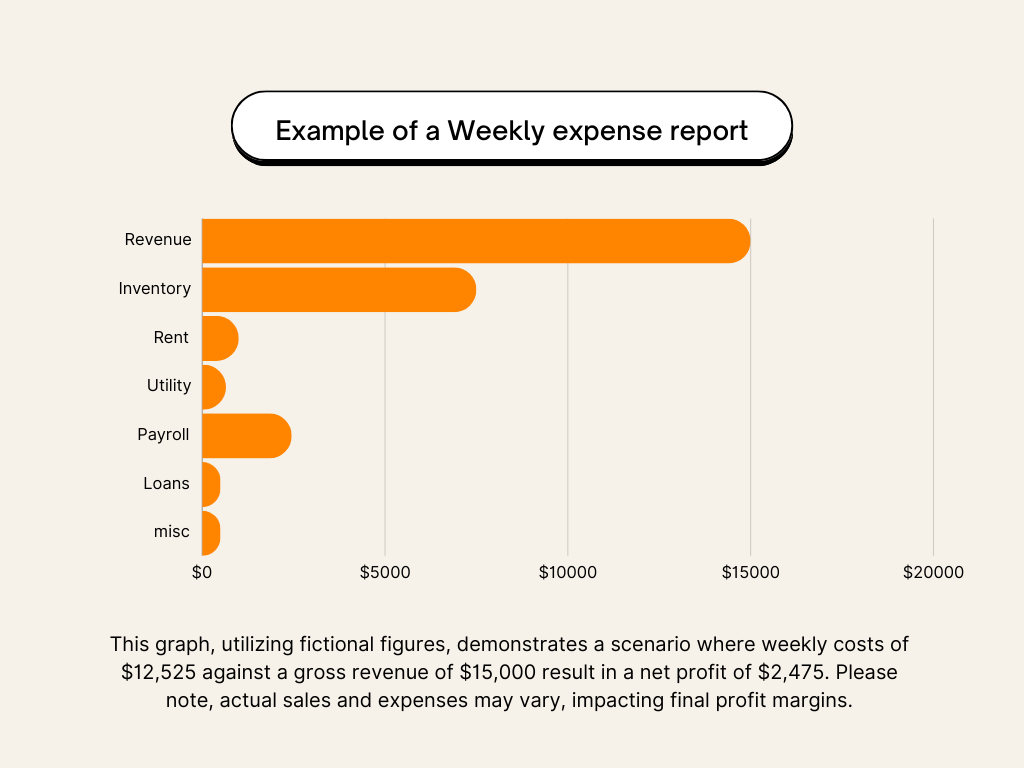

Here is how to handle this if you happen to buy a business and use up all your funds. Let's use a small grocery store you acquired as an example. I recently spoke to someone who owns a grocery store around me, and this is what he told me: A grocery store business requires planning ahead when it comes to paying rent, paying bills, and buying inventory from a large variety of distributors. He even said the only days he doesn't buy inventory are usually Sundays. Let's break down the numbers!

So, as you see in this example, it's always smart to have some backup emergency money just in case you have an emergency like broken equipment. This illustration shows you could have a net left of $2500, but is that enough?

4. Non-Compete in Place - Due Diligence in Business Acquisition

This one, I bring up often to many people who ask me for advice on buying a business, and many new buyers regret this after. It rarely happens, but when it does, it can be a serious issue, but avoiding this is very simple. It's called a non-compete agreement, which prevents the seller from ever competing with you after the transitions. Make sure to ask about this before signing on the dot.

5. Is It Valued Correctly - Negotiating Business Purchase

Negotiating a Business Purchase requires skills and patience. This is where lawyers and business brokers can step in. They will negotiate on your behalf, look for any red flags, and try to get you the best deal ever before you sign the deal. Negotiating can be a form of many things, from the asking price to the inventory in the business, and even lease terms, so I highly recommend hiring a business brokerage or lawyer for this.

6. Are the Employees Staying - Securing the Investment

Another important aspect is the employees and managers in the business; are they staying or leaving? You don't want to take over a business and the following week they walk out! Also, you want to blend in after the transition. Earning the trust of your new employees is vital to succeeding, as they say, “if you take care of your employees, they will take care of your customers.”

7. When Does Training Start - Transition Planning for New Business Owners

Transition Planning for New Business Owners should include a detailed training schedule starting as soon as the purchase agreement is finalized. This training, ideally conducted by the previous owner, ensures you understand all aspects of the business operations, from product knowledge to customer service protocols. A well-planned transition phase is crucial for maintaining the business's operational integrity and customer satisfaction.

8. Are There Any Contracts with Vendors, Supplies, or Distributors

Reviewing existing contracts with vendors, suppliers, and distributors is an essential part of the due diligence process. These agreements outline the terms of business relationships and can significantly affect the operation's cost structure and efficiency. Ensure these contracts align with your business goals and strategies for a smooth operational handover.

9. What Are the Lease Terms - Reading the Fine Prints

Understanding the lease terms of the business premises is crucial, as this impacts your long-term operational capacity and costs. Review the lease agreement for duration, renewal options, and any clauses that could affect your business operations or financial planning.

10. What Licenses Are Needed to Operate the Business

Identifying what licenses and permits are needed to legally operate the business is a critical step that should not be overlooked. The requirements can vary significantly depending on the industry and location. Ensuring you have all the necessary legal documentation from the outset is essential to avoid any operational or legal issues down the line.

The Elephant in the Room

I am not a broker, but I have acquired and sold many businesses, and I am using my experience as a way to help you understand a bit more than before you read this guide. You can find many business brokers that will be able to assist you in buying an existing business for sale, and I did too. This doesn't mean you cannot do it on your own, but this allows you to help ensure you are getting someone to negotiate on your behalf, work on financing terms, if any, and also get you a good lease agreement. Business brokers are good at spotting red flags, which you may miss.